1. Renters insurance doesn’t cost a lot.

Renters

insurance

with actual cash value will pay out based on the current value of an item. So, if you bought a laptop worth $1,000 five years ago and it was stolen now, you’d get a lot less than that. Renters insurance with replacement cost, on the other hand, will reimburse you for the cost of replacing the item. This means that should you ever need to replace that laptop, you’ll get $1,000 to do so.

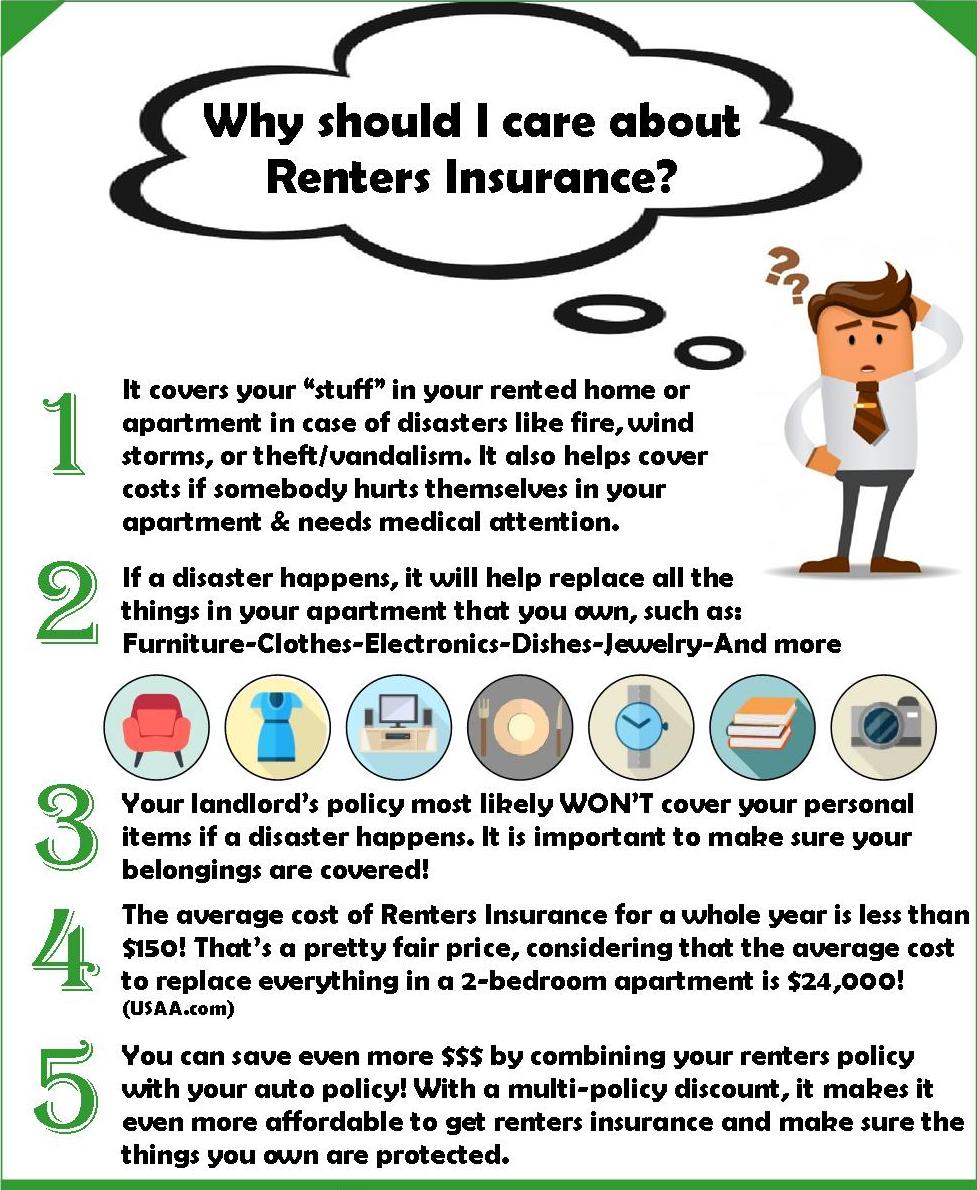

More and more people are living in rented apartments or homes. If you are one of them, whether you are renting a small apartment in the city or a spacious one in the country, you’ll need to protect yourself and your possessions by securing renters insurance. Now you might be thinking, why do you need renters insurance when the landlord is sure to have a property insurance policy? your landlord’s property insurance policy only covers loss or damages to the property itself. It does not cover loss or damages to your personal belongings. Even if you don’t own much, the cost needed to replace your items can accumulate to a lot more than what you would be willing to pay out of pocket.

Usaa is another great choice for renters insurance, and actually the company that i personally used while i was in college. The big drawback to usaa is that you have to be a member - and that requires that you serve in the military or are a dependent. While this does apply to a lot of people, it doesn't apply to everyone. Usaa offers renters insurance for as low as $5 per month. You can also combine this with other insurance and get a multi-policy discount - which could save you more than the cost of the renters insurance, making it free.

3. Renters insurance covers your stuff even when it’s not in your home.

Renters insurance is financial protection for people who rent the home that they live in. It covers personal property damage, personal liability, and loss-of-use. If your renters insurance is insurance for people who rent the home they are living in — whether it is a house, apartment, condo, or room share. If you pay a rental fee to a landlord or property manager (usually monthly), then you should consider purchasing a renters insurance policy so you have coverage for your belongings and personal liability. You don’t even have to be on a lease to qualify for a renters policy.

Basic tenant or renters insurance policies typically include three different types of coverage: contents: this covers your personal items. Be sure to discuss what items are covered in basic content coverage before purchasing any policy. In some cases, it may not cover all your valuable items (like jewellery and collections, which are subject to limits). Liability: tenant liability insurance protects you if you’ve damaged property, or an accident occurs in your home, and someone is injured. Most basic insurance policies cover $1 million to $2 million dollars in liability if a lawsuit is brought against you. Be sure to confirm liability coverage with your policy.

Do i really need renters insurance? yes, and this coverage is highly recommended. Most parents think that their homeowner’s policy covers their dependents, however, most are unaware of the policy caps for off-premise losses. Typically, only 10% is allocated in for off-premise losses and is often not enough to fully replace the possession(s) in the claim. Can i get renters insurance if i live with my parents? you can get a renters insurance policy without a lease and as long as you do not own or partially own the home. While many dependents have coverage under their parent’s homeowners policy, the coverage limits are generally not enough.

7. Renters insurance covers damage you cause.

Are you protected if a disaster hits your rental home? where will you go if repairs need to be made to your apartment before you can safely live there? what if your furniture and personal items are destroyed? many people think that their landlord or their landlord’s insurance will help them. This is not usually the case. The landlord will often have hazard insurance on the property. This insurance policy covers the structure, the building, but not the property inside. The landlord’s insurance policy will pay the landlord if the building is damaged and needs to be repaired. However, it will not pay for the tenant to replace their personal property or to find another place to live while the repairs are being made.

Aircraft renters insurance policies are primarily designed to protect you from liability damages incurred with the added risks of flying aircraft that you don’t own. Many pilots think that that their flight school or fbo has insurance that covers pilots renting their aircraft, but their insurance policy typically covers their interests in the aircraft and protects them against liability claims.

Policies vary somewhat from insurer to insurer, but there are three coverages that are standard on most renters insurance companies before the add-ons begin: 1. Personal property is everything owned by your renter which isn’t part of your physical property. This can range from furniture to electronics to jewelry and in some cases even pets. If items such as stoves, refrigerators, water heaters, etc. Are owned by you but operated by your tenants, make sure these items are covered under your landlords insurance policy. 2. Personal liability covers unintentional or accidental mishaps that occur to someone else or their belongings while in or on your renter’s property.

Consider the following possible mishaps that could occur in your home: you accidentally leave water running in your apartment’s kitchen sink. It overflows and damages the apartment below yours. Your friend comes to visit your condo, trips over your kitchen rug, and breaks her collar bone. Your usually friendly little dog bites a caregiver at your assisted living center. You may assume that none of these things will happen to you. However, if they do, have you considered who would be responsible for the medical bills or paying to repair the damages? if you’re a renter, it’s not your landlord — it’s you.

What is renters insurance and why should I consider it?

Question: my landlord sent me a notice stating that when i sign my next lease renewal i must provide proof of renters' insurance and that i must have certain minimum limit on personal property ($20,000) and personal liability ($100,000. ) the landlord must also be named as secondary insured. Is this requirement legal? what implications does it have for me in the event of a claim or lawsuit? griswold: the landlord can legally require you to provide proof of renters' insurance as a condition of your lease. Your landlord can also specify the minimum amount of coverage and require that the legal owner of the property and the property manager be named as an additional insured.

Insurance is oftentimes considered a financial “necessary evil. ” that’s because even though no one likes to pay any type of insurance premiums, when the time comes to file a claim, the benefits that are received are a welcome relief. So, as an investment property owner in florida, are your tenants required to purchase renters insurance? in a word, the answer to this question is no, tenants are not required by law to have this type of coverage. That being said, though, making the purchase of renters insurance a requirement in your lease(s) can help both you and your tenants to ultimately reduce potential out-of-pocket costs if something should happen to their belongings.

The three main coverage types provided by a renters policy are personal property coverage, personal liability coverage and loss of use coverage. Each of these coverages provides distinct protections: personal property, protects belongings that are owned by a tenant. This may be a wide range of items. Tenants personal contents such as clothing, furniture, electronics and even books are among many possible belongings covered. Liability insurance, helps shield tenants from certain liability suits arising from bodily injury or damage to someone else’s property. Loss of use, provides coverage for a tenant that may incur additional living expenses if displaced due to a covered loss.

Renters insurance is specifically designed to protect your personal property if it is damaged or stolen. Renters insurance can cover fire and smoke damage, theft, vandalism, damage from windstorms and hail, water damage from plumbing problems, and many other hazards. Renters insurance also provides liability and medical payments coverage in the event a guest is injured in your home. You probably own a great deal more than you think. What would the cost be of replacing everything in your apartment if there were a fire or other disaster?.

What does renters insurance cover?

Renters insurance is typically very affordable – sometimes as low as $20 per month – but it can save you from financial devastation in the event of a covered loss/claim, like a fire and other reasons. In some cases, landlords and property managers require that their tenants carry this coverage. However, even when it’s not required, its affordability makes carrying this coverage a no-brainer.

By jennifer langford | your money if you are a renter, it is critically important that you have renters insurance to protect you in the event of a theft or fire. Unfortunately, renters insurance does not receive the attention that it deserves! your landlord’s insurance does not insure your belongings, should an unfortunate incident occur. It covers the property only. Some people mistakenly believe that renters insurance is expensive; however, it’s no more than $30 a month and often cheaper if you shop around. Renters insurance will cover all of your personal property, medical bills, personal liability, and temporary living expenses.

Comments

Post a Comment