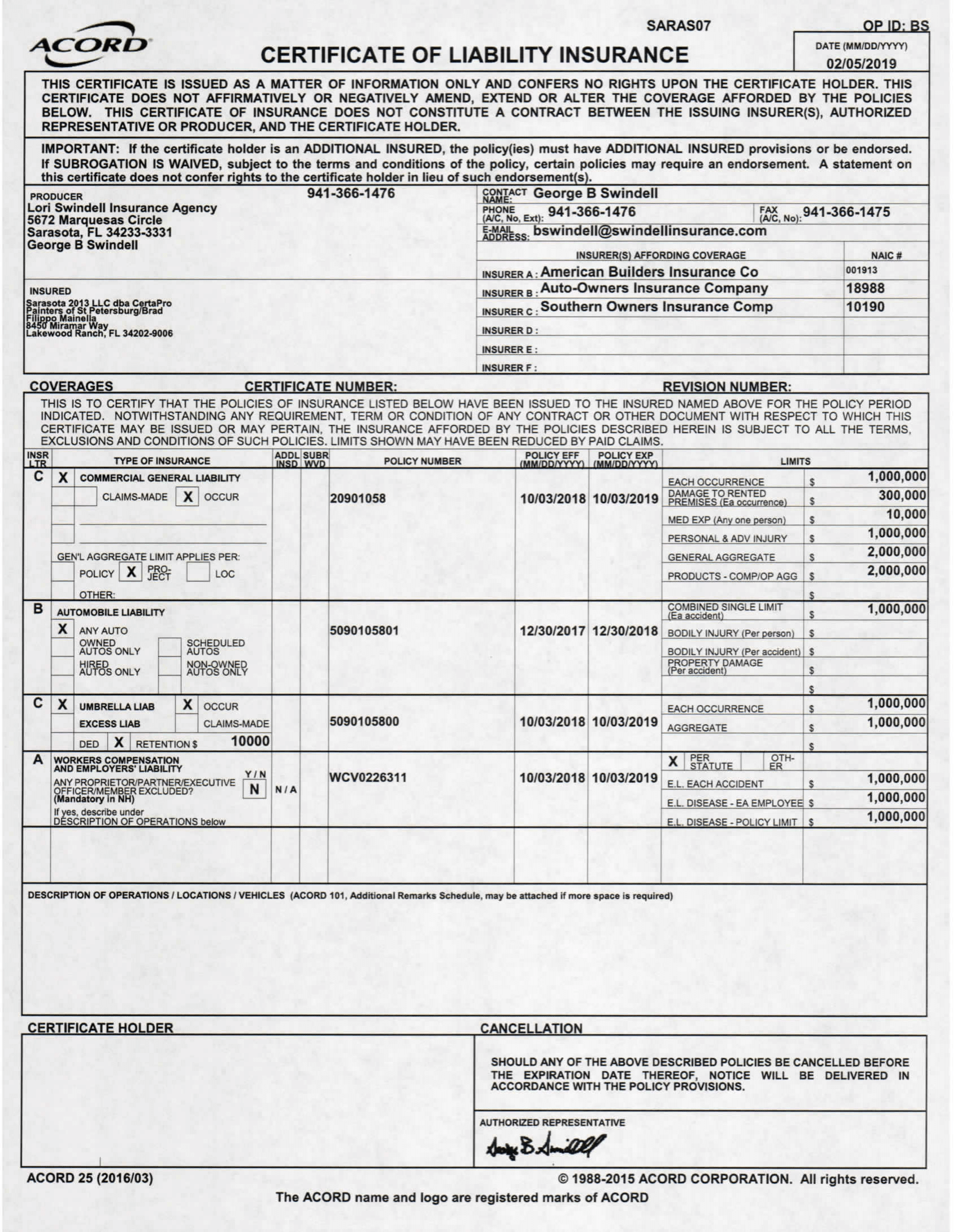

How Much Does General Liability Cost?

You have two ways of getting general liability

insurance

and each has its pros and cons.

Sometimes, an employer/client will add you on as an additional insured. Sometimes, the client may put you on their policy as an additional insured but it's more cost effective for the client to ask that you buy your own general liability coverage. If this type of insurance is required of you before you begin work, you can buy a competitive rate for general liability insurance quotes by visiting here. You always want to shop rates or have a trustworthy source like smartfinancial help you compare quotes before you choose.

Sometimes, an employer/client will add you on as an additional insured. Sometimes, the client may put you on their policy as an additional insured but it's more cost effective for the client to ask that you buy your own general liability coverage. If this type of insurance is required of you before you begin work, you can buy a competitive rate for general liability insurance quotes by visiting here. You always want to shop rates or have a trustworthy source like smartfinancial help you compare quotes before you choose.

General liability insurance protects you against a variety of claims. Consider the following two examples: if a client or customer slips and falls while visiting your business, general liability insurance will cover their medical expenses. It protects a customer’s house or property from harm caused by one of your employees. This liability insurance provides coverage that helps protect your small business from claims that come from your normal business operations, such as: property damage defense costs personal and advertising injury in most cases, general liability insurance coverage must be in effect at the time of the injury or damage to provide protection. Even if you stop paying premiums, they may still be able to give retroactive coverage.

General liability insurance covers legal and settlement costs if someone accuses your business of causing property damage, personal injury or harm to someone’s reputation. It can also cover medical payments for injuries that happen on your property, even if a legal claim isn’t filed. Specifically, commercial general liability insurance policies can pay out in cases of: third-party bodily injuries that occur on your property or as a result of an interaction with your business or employees. (this does not include injuries sustained by employees. )third-party property damage, or damage to someone else’s property caused by your business or its employees.

From traumatic brain injuries to litigation funding, several risks are complicating the liability landscape for businesses. Whatever challenges are on the horizon, our general liability (gl) coverage can help manage costs that your business could be required to pay as the result of lawsuits related to: and because each industry harbors different risks, we offer tailored protection to address your business’ specific needs. Whether someone trips in your parking lot or claims your product caused an injury, you’ll be better protected against out-of-court settlements, litigation costs, and court judgments.

What Does Liability Insurance Cover?

How much does a general liability insurance policy cost? how do i know how much coverage my company needs?

we help owners like you determine the right insurance policy that balances the best combination of price and protection for your business—from product liability and cyber liability to errors and omissions. The cost and rate of a general liability insurance policy is based on your unique business risks and coverage requirements. Call us for more information or find a local insurance agent to get started on your personalized quote.

If we already have business liability insurance, why would i need commercial umbrella coverage?

basically, commercial umbrella liability insurance picks up where your primary liability policy leaves off.

If we already have business liability insurance, why would i need commercial umbrella coverage?

basically, commercial umbrella liability insurance picks up where your primary liability policy leaves off.

When customer property is damaged by an employee, your general liability insurance coverage may pay for a replacement. For example: your contractor accidentally sets fire to a building they are working in, and repair costs will exceed $150,000. Now, you may be liable to pay for the damages and construction costs. With small business liability insurance from biberk, you would likely have help covering the costs of those damages. Bodily injury if someone other than an employee is injured on your property, general liability insurance coverage can take care of medical expenses plus legal expenses and damages. If products developed or sold by your business harm people or property, small business liability insurance can pay legal expenses associated with product liability lawsuits and medical expenses if an injury occurs.

General liability insurance is coverage for claims that may be filed against your business. This could include claims of property damage, reputational harm, advertising injuries, and bodily injury. If you didn’t have this type of policy and someone was injured during your regular business operations, you may have to cover the costs out of pocket instead. Some business owners purchase this coverage as a standalone policy, and others will include it as a bundle in their business owners policy. General liability insurance does not cover professional service mistakes, damage done to your own commercial property, or employees who qualify for workers’ compensation.

General liability insurance covers three categories of damage: property damage, bodily injury, and personal and advertising injury. Under cgl, your insurer will cover the costs of any legal defense or attorney’s fees incurred while defending against covered lawsuits, as well as any medical payments. In the event that your business is sued because of an accident, cgl can help provide financial backing to help reduce the financial strain on your business.

What Does a General Liability Policy Cover?

General liability business insurance covers financial costs if your business is responsible for non-professional negligent acts such as property damage, bodily injuries or advertising harm caused by your services. This coverage can be found as a standard part of both a business owners policy (bop) and commercial package policy , and it can protect your business from paying legal fees and damages if you’re found liable.

If someone falls while visiting your business premises, or a customer is hurt by a product your business sells, you can be held responsible. That's the risk that liability insurance covers. Liability insurance, also called commercial general liability (cgl), covers four categories of events for which you could be held responsible: bodily injury; damage to others' property; personal injury, including slander and libel; and false or misleading advertising. Cgl coverage pays for the injured party's medical expenses. It excludes your employees, who are covered by workers' compensation. (for details see workers' compensation section of this site. ) bear in mind that even trespassers can sue you if they fall and get hurt on your business premises!.

General liability insurance, or business liability insurance, is a type of insurance that helps to defend your business from claims such as bodily injury or property damage that arise from your business operations. This type of policy could include coverage for property damage, medical expenses, legal costs and more.

General liability insurance is a commercial insurance policy that protects your business from a wide variety of risks. Considered to be the first type of insurance policy you should look into when establishing your business, general liability helps you after an accident occurs either on your property or off. Maybe someone falls on your commercial property, or you find yourself in a copyright infringement lawsuit. General liability can be there to help support you after a variety of accidents.

What Does General Liability Insurance Cover for a Small Business?

A commercial general liability (cgl) insurance policy provides indemnity against the risks that nearly all business owners face. It protects your business assets from any claims of injury related to your business and responds to claims of negligence made by a third party. The court costs alone from even one lawsuit could be financially devastating to most growing businesses. Commercial general liability insurance can provide you with legal defense (per occurrence aggregate applies to settlements only) and with the resources to keep your business operating even in the midst of a lawsuit. Most cgl policies also include some form of product liability coverage.

General liability insurance is a type of commercial liability insurance policy that protects a business from the financial burden of claims arising from bodily injury, personal injury, or property damage. Risks typically covered by a general liability business insurance policy include: bodily injury (physical damage to a person’s body, non-employees) property damage (injury to real or personal property, whether your property or a client’s) medical payments (resulting from accidents that happen on your premises) personal liabilities (libel, slander, copyright infringement, invasion of property and privacy, wrongful eviction, false arrest) advertising liabilities injury (losses caused by your advertising or by violating another company’s copyright) legal defense and judgment.

While general liability insurance protects you, your business, and your employees in the case of bodily injury, property damage, or personal injury claims, small business owners should consider other types of insurance: workers’ compensation insurance provides medical, disability, survivor, burial, and rehabilitation benefits to employees who experience illness, injury, or death due to a work-related incident. In nearly all states, and with few exceptions, businesses are required by law to carry workers’ compensation insurance. Get a workers’ comp quote in 3 minutes. Commercial auto insurance covers liability and physical damage for vehicles owned by your company. Cyber insurance protects your business against data breaches and cybercrime such as computer hacking and stolen information.

General liability insurance protects contractors and small-business owners against claims of bodily injury claims, medical costs, and property damage. It is often bundled with business liability insurance or property insurance but can also be purchased as a standalone policy. General liability insurance covers the following: bodily injury and property damage, lawsuits, medical, personal injury, contract liability, and more.

What Does General Liability Insurance Not Cover?

Your business faces liabilities every day. The only way to protect your assets is to carry adequate business liability insurance. A general liability insurance program can include a blend of traditional insurance and alternative risk financing mechanisms to help manage a company’s liability risk.

General liability and/or product liability insurance is necessary for a business because every operation is responsible for its products, services, and the conduct of its employees. General liability insurance protects your business against financial loss resulting from claims of injury or damage caused to others by you or your employees. Regardless of whether you manufacture products, deal in intellectual property, or provide some type of service, you need liability insurance to protect you from third-party claims for bodily injury, property damage, personal injury, or advertising liability: bodily injury liability: protects your business from paying for damages if a third-party should become injured on your premises or injured as a result of using one of your products.

Shelter's general liability insurance can help you pay for bodily injury and property damage that you are legally liable to pay.

The commercial general liability policy premium is based on a variety of factors, depending on the types of coverages included. The size of the insured’s operations and the inherent risk of the products will impact the premium.

Comments

Post a Comment