Ladder Life Insurance Review 2022

In order to purchase most life

insurance

policies, applicants may be required to undergo underwriting. Underwriting is a process that life insurance companies use to determine the degree of risk a potential client may pose before assuming that risk and providing coverage. The underwriting process typically involves and underwriter reviewing a potential insured’s insurability, including reviewing information about the insured’s current and past health, as well as other factors. Although traditional underwriting can be invasive and time-consuming, brighthouse simple underwriting can simplify the process for some brighthouse financial (bhf) products.

Our process generally requires no labs or medical exams and often provides an expedited response generally within 24 hours for applicants meeting certain criteria.

Our process generally requires no labs or medical exams and often provides an expedited response generally within 24 hours for applicants meeting certain criteria.

When you apply for life insurance, the insurance company underwriters review your health and lifestyle factors. After their evaluation, they assign you to a risk class. If there are certain factors that place you outside the normal range of risk the insurance company typically insures, you may be considered substandard.

Aflac Life Insurance Review 2022

Choosing the right life insurance policy is important.

At aflac, we offer a variety of life insurance plans to help meet your

specific

needs.

At aflac, we offer a variety of life insurance plans to help meet your

specific

needs.

Best No-Exam Life Insurance Of July 2022

Many factors may come into play when deciding which type of life insurance will suit your needs. The best thing to do is to speak with a qualified insurance professional who can help you examine these factors, so you can determine which type of coverage may be appropriate. 1. Investopedia. Com, march 3, 2022 2. Investopedia. Com, may 23, 2022 3. Investopedia. Com, august 31, 2021 4. Investopedia. Com, march 2, 2022 the content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties.

Term life insurance offers financial protection for a set time frame, generally ranging from 10-30 years. Term life insurance is generally the most affordable type of insurance and is a great option for younger families, business owners and single individuals. With term life, you’re “renting” life insurance coverage for a set period. For example, if you purchase a 20-year term life policy for a face value of $50,000, pay your premiums on time, and pass away after 15 years, your chosen beneficiary will receive a death benefit of $50,000. Your beneficiary will be able to decide how the money from your death benefit is spent; this money could go towards funeral and burial costs, remaining mortgage expenses, funding your child’s college education, or donating to a local charity.

You're not automatically disqualified from getting life insurance if you have a pre-existing condition. For example, if you have diabetes, elevated cholesterol, or blood pressure issues, an insurance company may simply evaluate these conditions differently when assessing your overall health risk. Here are a few common questions an insurer might ask to help determine the type and amount of life insurance they'll offer: is your condition under control? do you take medication to manage your condition? do you see your doctor regularly? have you had a recent health issue that caused you to see a doctor, get additional testing, or receive treatment?.

Term life insurance is meant for anyone that wants to get coverage over a certain period. For example, you can get a term life insurance policy for 10 years. The money would be distributed to your beneficiaries if you died within the next 10 years. This is a great option if you’re worried about your health and want to save as much money as possible. However, you may end up spending more money than you would on another policy if you extend the term.

Best Term Life Insurance Of July 2022

Whole, variable universal, term, and more. Life insurance can be confusing and keeping the different types straight can be tough. In general, life insurance guarantees a death benefit to a designated beneficiary after a policyholder dies. Like most policies, life insurance requires a recurring payment known as a "premium" to keep the policy active. Ready to learn more about life insurance? let's dive in.

It provides coverage for a set period (usually 10-30 years). Should you die within that period, your beneficiary will get a death benefit. Typically, the premium payments and death benefit on a term policy are fixed from the start, and the premiums are much lower than those of permanent life policies. When the term of coverage ends, you may be offered the option to renew the coverage for another term or to convert the policy to a form of permanent life insurance. 4.

We've been helping people secure their financial future and protect the ones they love more than of life insurance protection in force as of 12/31/21 named for the year in a row as a best place to work for disability inclusion according to the disability equality index® delivered in life insurance and annuity benefits paid in 2021 what's behind massmutual's financial strength 1 access to cash values through borrowing or partial surrenders will reduce the policy's cash value and death benefit, increase the chance the policy will lapse, and may result in a tax liability if the policy terminates before the death of the insured. 2 dividends are not guaranteed.

Term life insurance provides protection for a 10-, 20-, or 30-year period. Rates are based on issue age and are guaranteed to remain level during the initial term period you choose. Term life insurance does not have the flexibility of cash value.

Best Life Insurance Companies Of July 2022

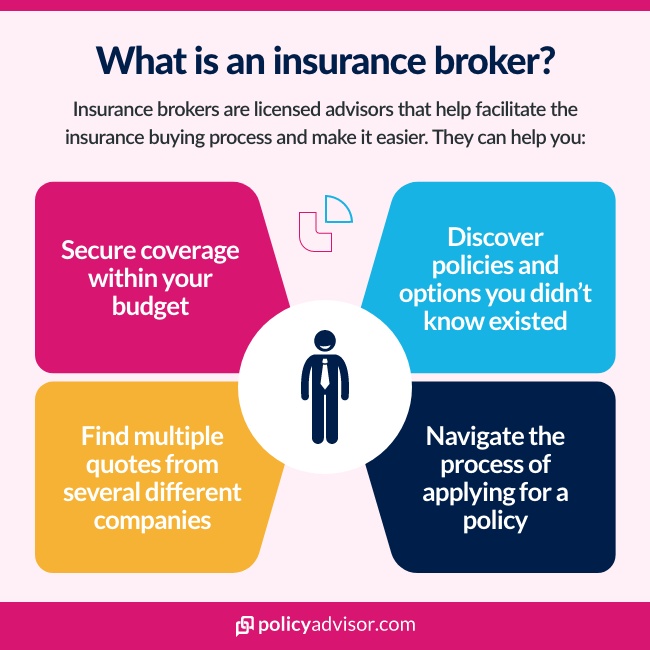

If you are unhappy with the table rating offer you received, there are 2 options. Reconsideration request this will depend a lot on the specific reason or condition that led to the table rating. Life insurance carriers have certain time frames that they “penalize” you for. As time passes without complications or additional issues, you outlook improves. Table rating due to a recent dui ? as 12 or 24 months have passed, you can find lower rates. Table rating with a stroke from 2 years ago? if symptoms have improved, you can get a better rating. Your independent broker can help you file a reconsideration request.

Dividends reflect a mutual insurance company’s profits over a predetermined period. Profits include funds from interest and investment returns, as well as the number of new policies the company sold. Your share of the payout depends on how much you’ve paid into your policy. Example: if your policy has a value of $100,000 and your mutual insurance company offers a 5% dividend, your annual dividend would be $5,000. If, in the following year, your payments increased the value of the policy to $120,000, your annual dividend that year would be $6,000. When considering top mutual insurance companies guardian, penn mutual, lafayette life, and massmutual, the average dividend payout for 2021 is estimated to be 5.

As we mentioned, a participating whole life insurance policy is eligible to earn dividends. Generally speaking, a dividend is nothing more than earnings that a company distributes to policyholders. Not all companies offer participating whole life insurance policies. Many years ago, every insurance company had a participating policy, but that trend has changed. Most insurance companies focus on term insurance, which is great for providing you with a large death benefit for an affordable price. Here are a few things you need to know about dividends: you can use dividends to reduce future premium payments. Dividends help the policy growth you can use dividends to purchase additional coverage.

The maximum age at which you can purchase a life insurance policy varies from company to company. However, you may only be able to buy a life insurance policy up to the age of 85. Most insurance companies consider people above 85 years old uninsurable.

Comments

Post a Comment