What type of coverage are you looking for?

While rates of life

insurance

ownership have fallen, the face value of policies has increased for both term and cash value insurance. This is the case both in absolute terms and when measured in terms of the number of years of household income represented by the face value of the policy (see table 2).

The average face value for term life insurance measured in 2013 dollars climbed from $155,996 in 1989 to $353,288 in 2013, a 126. 5 percent increase. 8 over the same period, the average face value for cash value life insurance increased from $157,902 to $225,894, a 43.

The average face value for term life insurance measured in 2013 dollars climbed from $155,996 in 1989 to $353,288 in 2013, a 126. 5 percent increase. 8 over the same period, the average face value for cash value life insurance increased from $157,902 to $225,894, a 43.

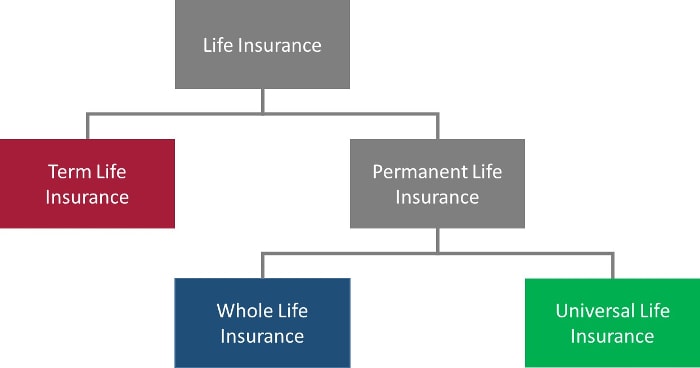

For the most part, life insurance fits into one of two classes: permanent life insurance and term life insurance. There are many variations within these classes. Imagine insurance advisors can help you sort through your options to determine which type and what amount of coverage is right for you.

The average cost for life insurance is less than $50 a month, according to our price analysis of 14 different life insurers across different ages. For example, a $500,000, 20-year term life policy for a healthy person between ages 25 and 40 costs around $28 a month. However, your rate depends on many factors like your age, gender, health, job or smoking habits. The coverage amount, term length and the type of policy come into play too. Insurers weigh factors differently, which is why it’s important to compare quotes from multiple companies.

Whole life insurance ,or permanent life insurance, is among the most common types of insurance in canada. It provides coverage for your entire life, as long as you pay the premiums on time. For this reason, whole insurance also goes by the name of permanent life insurance policies. Besides promising a set payout whether you die young or old, a whole life policy includes an investment feature. A portion of your each premium payment gets deposited into a saving component called “cash value”. Your policy’s cash value grows with interest over time and acts as a financial net to fall back on during uncertain times.

Group life insurance is a type of life insurance coverage in which a group is the master policyholder of an insurance contract, and certificates of insurance are issued to participating individual members. These insurance policies are most commonly offered by employers to their employees as a free or optional benefit. Entities such as organizations, trade groups, and associations also can offer group life insurance to their members. It is available to people of all ages, and there are few health questions, if any, that must be answered in order to qualify. Term and whole life policies may be available, depending on the group.

What is life insurance?

In order to sell life insurance, a financial professional must be a properly licensed and appointed life insurance producer.

1 for federal income tax purposes, tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death (any outstanding policy debt at time of lapse or surrender that exceeds the tax basis will be subject to tax); (3) withdrawals taken during the first 15 policy years do not cause, occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract.

Ordinary life insurance is a type of life insurance in which policyholders pay premiums for their whole lives at a set price and interval. However, ordinary life insurance policies are often considered paid up if the policyholder reaches 100 years of age. Ordinary life insurance is a term that is often used interchangeably with "whole life insurance. "advertisement insuranceopedia explains.

By john nichols on june 28, 2021 in financial planning by: bill few associates senior vice president, john nichols, cfp® today is national insurance awareness day, and while a discussion on insurance is not the most interesting of topics, understanding how it works and why it may be necessary is vital to your personal finances. This is especially true for life insurance. So, since this is national insurance awareness day, let’s take a moment to review the details of life insurance including the most common policy options, term and whole life, and how each can affect your financial situation. First, let’s review term life insurance.

Price (50% of score): we averaged the no-exam life insurance rates for males and females in excellent health at ages 30, 40 and 50 for $500,000 and $1 million and a term length of 20 years. Maximum face amount for lowest eligible age (10% of score): companies with higher no-exam life insurance coverage amounts for the lowest age earned more points. Note that maximum no-exam coverage can sometimes become lower if you apply at a higher age. Age eligible for best length/amount (10% of score): companies offering no-exam life insurance to folks over age 50 earned extra points. Accelerated death benefit available (10% of score): this important feature lets you access part of your own death benefit in the event you develop a terminal illness.

It seems like every day there is a new “big idea” for shielding both wealth and income from the long reach of the internal revenue service. Surprisingly, the latest hot take on tax reduction and wealth protection centers on an investment most people consider about as trendy as an over-60 men’s bowling league: it’s called life insurance. Types of permanent life insurance policies whereas term life insurance offers only a death benefit that diminishes over the years, a permanent life insurance policy offers a guaranteed death benefit and builds cash value over time. In the case of whole life insurance, accumulating cash value comes solely from paid-in premiums.

The cost of life insurance

Cash flow banking is a concept that allows you to capture the opportunity cost of your dollars. It lets you be your own bank and earn interest on yourself. This is most commonly achieved using dividend-paying whole life insurance. Whole life insurance is used because it’s safe and financially strategic. Here’s why.

Your child would pay the same child-size monthly premium rate for life even after becoming the policy owner at age 21. All your child needs to do is keep paying the premiums. This is a huge benefit, given that age affects life insurance premium rates. For example, buying a life insurance policy at age 50 versus age 30 could cost three times as much. 1 by having grow-up® plan protection with a locked-in premium, your child won’t have to worry about rising costs. The sooner you apply for the grow‑up® plan, the lower the premium rate.

Term life insurance offers financial protection for a set time frame, generally ranging from 10-30 years. Term life insurance is generally the most affordable type of insurance and is a great option for younger families, business owners and single individuals. With term life, you’re “renting” life insurance coverage for a set period. For example, if you purchase a 20-year term life policy for a face value of $50,000, pay your premiums on time, and pass away after 15 years, your chosen beneficiary will receive a death benefit of $50,000. Your beneficiary will be able to decide how the money from your death benefit is spent; this money could go towards funeral and burial costs, remaining mortgage expenses, funding your child’s college education, or donating to a local charity.

Group life insurance policies

Have questions about protecting your family? why do i need life insurance? do i need life insurance if i'm single? 1 policy loans and withdrawals will reduce the cash value and death benefit of the contracts. Clients may need to fund higher premiums in later years to keep the policy from lapsing. Under current federal tax rules, you generally may take income tax-free partial withdrawals under a life insurance policy that is not a modified endowment contract (mec), up to your basis in the contract. Additional amounts are includible in income. The irs places a limit on how much money can go into life insurance premiums for the policy and how quickly such premiums can be paid in order for the policy to retain all of its tax benefits.

Quick action calculate term premium tata aia life insurance company ltd. (irda regn. No. 110 ·cin:u66010mh2000plc128403. Registered & corporate office: 14th floor, tower a, peninsula business park, senapati bapat marg, lower parel, mumbai 400013. Trade logo displayed above belongs to tata sons ltd and aia group ltd. And is used by tata aia life insurance company ltd under a license. For any information including cancellation, claims and complaints, please contact our insurance advisor/intermediary or visit tata aia life's nearest branch office or call 1-860-266-9966 or write to us at customercare@tataaia. Com. Visit us at www. Tataaia. Com.

If your employer participates in the vrs group life insurance program, you are covered from the first day of employment. Your employer may pay your portion of the premiums for basic group life insurance coverage. If you are covered under the basic group life insurance program, you are eligible to purchase additional life insurance for yourself as well as your spouse and dependent children through the optional group life insurance program. You pay the premiums for this additional coverage through payroll deductions.

How the types of life insurance stack up

Insurance 23-07-2022 in this video, we will talk about three fundamental types of life insurance: ❎term life ❎permanent lie ❎universal life it … watch more new videos about insurance | synthesized by mindovermetal english.

Comments

Post a Comment